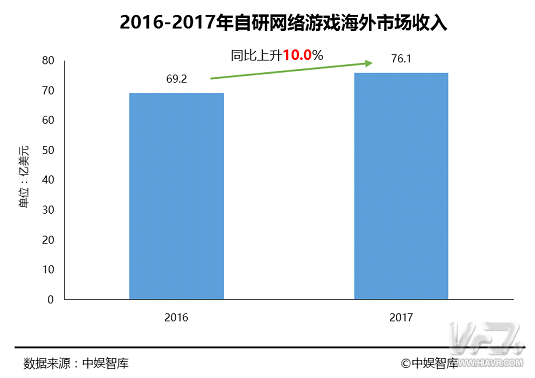

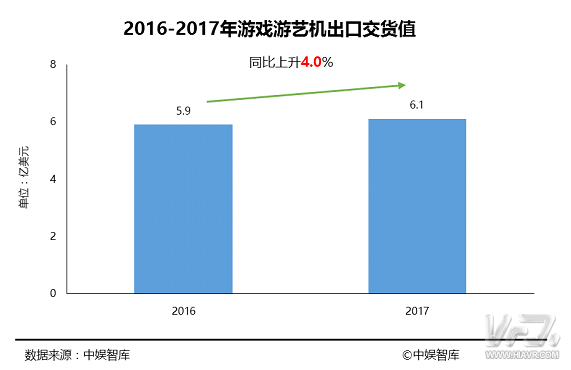

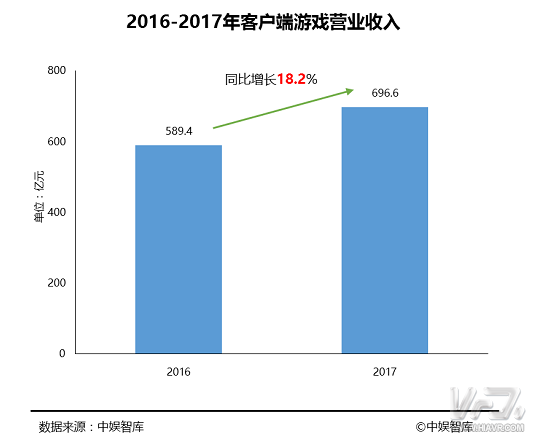

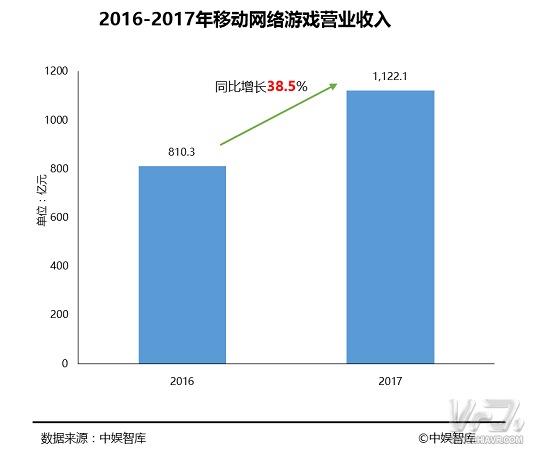

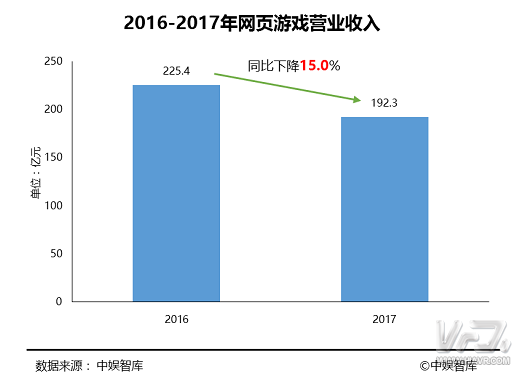

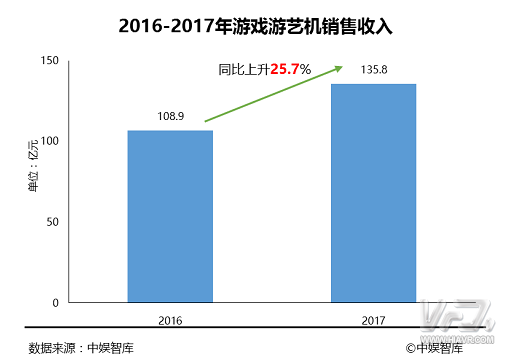

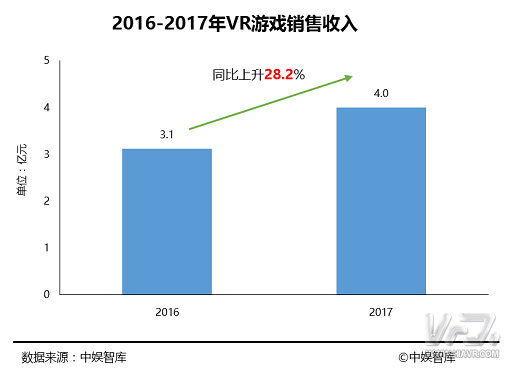

The China Culture and Entertainment Industry Association Information Center and China Entertainment Think Tank jointly released the “2017 China Game Industry Development Report†on November 28. This report will address the overall development of the Chinese game industry in 2017, the status quo of game segmentation, and the development of the game industry. The characteristics were analyzed and predictions were made on the development trend of the Chinese game industry. The report pointed out that social spending on game entertainment continues to increase, effectively driving the rapid development of game entertainment and home console industry. Overall, the gaming industry's operating income in 2017 has steadily increased. The report believes that the market scale of the game industry will continue to grow in the future. With the maturity of the mobile game market and the upgrading of concept of game users' consumption, the online game market still has great growth potential. The effective guidance of the government and the upgrading of consumer spending will continue to promote the development of quality games with content, innovation, and innovation. Full report: I. Overall situation of China's game industry in 2017 (I) Market Overview In 2017, the overall development of the game industry in China has remained steady. As mobile games enter the stock market stage, the increase has declined somewhat, which still has a greater driving effect on the overall growth of the industry. Social consumption spending on game entertainment continues to increase, effectively spurring the rapid development of game entertainment and home console industry. Overall, the gaming industry's operating income in 2017 has been steadily increasing. In 2017, the overall operating revenue of the game industry in China was approximately RMB218.96 billion, a year-on-year increase of 23.1%. Among them, online games contributed a lot to the operating revenue of the industry (the operating income in the first three quarters reached 151.32 billion yuan). It is expected that the annual operating revenue will be approximately 201.10 billion yuan, a year-on-year increase of 23.1%; the related revenue from home consoles will be approximately 3.88 billion yuan. , an increase of 15.1% year-on-year; Game Amusement Machine (first-quarter sales of 9.98 billion yuan) is expected to be 13.58 billion yuan for the year, an increase of 24.7%; VR games revenue of 400 million yuan, an increase of 28.2%. Specifically: With the improvement of hardware technology and the change of users' game habits, the internal structure of online games has become more differentiated: mobile games led by operating income of approximately RMB 112.21 billion for the year, a year-on-year increase of 38.5%, accounting for 55.8 percent of the market share of online games. %; Client game revenue was approximately 69.66 billion yuan, up 18.2% year-on-year, accounting for 34.6% of the online games market; web game revenue was approximately 19.23 billion yuan, down 14.7% year-on-year, accounting for 9.6 of the total online gaming market share. %. In 2017, self-developed online game revenue steadily increased, which was approximately 142.07 billion yuan, an increase of approximately 14.5% year-on-year. The home console market is still in its growth stage, and users' payment habits gradually develop. The operating income for the year was approximately 3.88 billion yuan, an increase of 15.1% year-on-year; the gaming and entertainment industry entered a period of rapid development, and the gaming amusement machine sales revenue was approximately 13.58 billion yuan. , a year-on-year increase of 24.7%. In 2017, VR game technology has further matured. A number of client games have launched VR versions, and game entertainment devices have actively introduced VR gameplay. However, the VR market still has large fluctuations. High-end VR devices have increased the consumption threshold. In 2017, sales revenue of VR games and equipment was approximately RMB 400 million, a year-on-year increase of 28.2%. (b) Overseas exports In 2017, China’s gaming companies had a high enthusiasm for going offshore. Self-developed online games’ overseas operating revenue was approximately US$7.61 billion, a year-on-year increase of 10.0%. In 2017, Chinese game companies have the following new features in the sea: First, the competition of “Chinese counterparts†in overseas markets is fierce, and mobile games in Southeast Asia tend to be homogenized; secondly, self-developed secondary mobile games have performed well in Japan and South Korea. Third, strong game companies have actively acquired overseas R&D and distribution companies and deployed global markets. In 2017, the gaming and entertainment industry will continue to develop along the path of transformation and upgrading, actively improve technology, innovate games, communicate and improve international competitiveness. In 2017, the export value of game amusement machines was approximately US$610 million, an increase of 4.0% year-on-year. (III) User Scale In 2017, the characteristics of the online market of Chinese online game users were obvious, and the growth rate continued to slow down. Among them, the number of client game users is about 150 million, which is basically the same as in 2016; the number of mobile game users is about 460 million, an increase of 9.0% year-on-year; the number of web game users is about 240 million, which is a year-on-year decrease of 2.0%. Although the number of online game users has slowed down, the proportion of core users has continuously increased, and the user's game aesthetics and genuine awareness have been promoted. This has provided good opportunities for independent games with high-quality games and innovative gameplay, and inferior games will gradually be eliminated from the market. In 2017, the number of VR game users was approximately 40 million, an increase of 100.0% over the same period of last year, and the number of consumers in the VR Experience Pavilion continued to increase; e-sport game users were approximately 220 million, a year-on-year increase of 69.2%, and the proportion of female players continued to increase. Second, the development of game segmentation in 2017 (a) Client Games In 2017, the Chinese client gaming industry developed rapidly. The annual operating income totaled approximately 69.66 billion yuan, up 18.2% year-on-year, accounting for 34.6% of the online game market. The main factors affecting income are: First, with the upgrading of game quality and consumer attitudes, the overall proportion of core users continues to increase, and the average per capita consumption of players has increased dramatically; secondly, the development of e-sports has led players to consume enthusiasm; third, traditional Popular games learn to improve the popularity of this year's popular "battle" gameplay. In the aspect of client game products, new online game manufacturers continue to decrease, and the degree of concentration is relatively low. The operator of the head-end game is highly centralized, and is basically a classic game or an overseas introduction game. Tencent and Netease have a relatively large market share. , New game testing (excluding games such as Steam platform games) throughout the year greatly reduced in frequency and quantity. In terms of client game users, the awareness of genuine users and the awareness of paying are constantly increasing, and the market demands are more diversified. In April 2017, the Tencent WeGame platform was officially released. In July, the Oriental Pearl New Media teamed up with Microsoft China and Hail Interactive to publish the G-Games platform. The competition in the client gaming platform has become more intense and has brought more vitality to the market. The US Steam platform operates in China through a cross-border payment model, which poses greater challenges to management and client game companies. In November, there were approximately 30 million players in the China area of ​​the Steam platform, which continued to maintain significant growth. This data also indicates that client games still have a large market potential in China. In 2017, the types of popular client games were highly concentrated, and the number of role-playing games occupies a major advantage, about 48%; MOBA games performed brilliantly. Although “League of Legends†was impacted by MOBA mobile games, its players The number, game revenue and social influence are still in the leading position in the client game. (b) Mobile Games In 2017, China Mobile’s annual revenue was approximately RMB 112.21 billion, an increase of 38.5% year-on-year, accounting for 55.8% of the online game market share. The main features of the market in 2017 are as follows: First, the long-term operational capabilities of classic games are strong. For example, “Glory of the King†still holds the first place in the best-selling list in 2017, and the top 5 of the best-selling list tends to be solidified. Most of them are classics such as Onmyouji and Fantasy Westward Journey. Games, the above-mentioned classic game's pan-entertainment operation effectively maintained the player's activity and product vitality. Secondly, the new model of gameplay has gradually improved and it has been recognized by the mainstream market. For example, "Happy Wolfman Killing" originated from board games, strong sociality and entertainment, and "Angel's Sword H5" using mature H5 technology. All were among the best sellers. Third, the game with the theme of the second element is favored by users. Starting from the "Yin and Yang Division," the "College of Disintegration 2" and the "Monthless" products have gathered a large number of users. The secondary meta platform has become a new one. Mobile game channels. In terms of product types, the mainstream game types in the market remained stable, the market share of role-playing games and casual educational games exceeded 50%, and strategy games ranked third. In 2017, about 16,000 new mobile games were launched. In the first half of 2017, the top three types of mobile games were: 31% leisure puzzles, 27% role-playing, and 14% strategy; and new products in the third quarter of 2017. The top three mobile game types were: role-play 30.6%, casual puzzle 26.9%, and strategy 13.7%. With respect to content supply, new IP-based games still have greater market competitive advantages. New role-playing IP games accounted for 55% of the total; the top three IP sources were: animation 42%, historical masterpiece 20%, and film and television works 18%. For IPs with a more complete view of the world, role-playing games are better at restoring IP plots and increasing player participation, which is conducive to maximizing the value of IP, such as "Chuoqiao", "Military Alliance", "Kyushu Sky City". The IP linkage of best-selling new role-playing games such as 3D is a success. (iii) Web games In 2017, China’s web game revenue declined significantly. Its annual operating income was approximately RMB 19.23 billion, a year-on-year decrease of 15.0%, accounting for 9.6% of the total online game market share. There are three reasons for the decline of web game operating revenue: First, the total number of web game companies and web games has decreased, high-quality web game companies have continuously increased their mobile game business share, and secondly, with hardware upgrades, users pursuing high experience tend to be clients. Games, the pursuit of game convenience users tend to mobile games, web game user groups continue to decrease; Third, web game game diversity and game quality are lagging behind the other two types of online games, it is difficult to meet the ever-changing market demand for games. In terms of gameplay, the legendary type of national warfare products still occupy the head market share. The classic legendary games such as Legend of the Blue Moon, Legendary Hegemony, and Archangel's Sword were generally better than new games in the market this year. With regard to content supply, the distribution of themes is more concentrated, and new games are favored by domestic popular film and television IP. In 2017, approximately 2728 web games were formally launched, of which magical and fantasy subjects accounted for 46.7% and 20.0%, respectively; high-quality movie tour linkage works achieved a high degree of market attention. In terms of the number of games opened, in 2017, the number of open services for head games on web games decreased, and the market concentration increased slightly. The non-headed products have a harsher living environment. On the R&D side, high-quality R&D companies accounted for a major market share. Head-manufacturers' revenues declined significantly compared to 2016, and head-end R&D revenues were more differentiated. (4) Game entertainment and home game consoles Game entertainment In 2017, the sales revenue of China's game amusement machines was approximately RMB 13.58 billion, which was a year-on-year increase of 25.7%. The operating entertainment venues in China had an operating income of approximately RMB 98.18 billion, an increase of 41.6% year-on-year. In 2017, the major growth of gaming entertainment equipment revenue is the demand for equipment in newly opened entertainment and entertainment venues, rapid replacement of equipment, and high prices for high-tech equipment that are welcomed by the market. In 2017, the income of China's entertainment and entertainment establishments was mainly affected by the following factors: The industry transformation and upgrading achieved remarkable results. While phasing out laggard establishments, the number of new chain stores increased, and the operating income increased significantly; the theme park stimulated the growth of sideline industry revenues (diet, Derivatives, value-added services, etc.; With the prevalence of e-sports and the concept of national fitness, the positive image of the industry has increased significantly, and the consumer groups in the area have expanded. In the first three quarters of 2017, about 532 new game entertainment devices passed the approval. In the third quarter of the overhaul models, children's entertainment, environmental experience, and e-sports models had the highest weight, and the proportion of gift lottery models was significantly reduced. Among them, the growth rate of e-sports and sports models is large, and it fits the trend of national fitness, reflecting the wave of high-speed development of e-sports. Home game machine In 2017, the sales revenue of home consoles (including supporting game consumption) was approximately 3.88 billion yuan, an increase of 15.1% year-on-year, and annual sales of home consoles were approximately 890,000 units, an increase of 12.0% year-on-year. The main reasons for the slight increase in sales revenue of home consoles are the following: First, with the general improvement of people’s living standards, society’s attitude towards gaming is more inclusive, and players are more valued for high-quality gaming experiences, the family’s willingness and ability to spend on home consoles have increased; Second, the low-end console market such as domestic bullies has performed well; Third, the sales revenue of console game content in the country area is low, and the number of games imported from the host country service is less than that of the outside service. The quantity is less and the price is more expensive. Domestic users get more open channels for out-of-gaming games, and a large number of users tend to spend on external clothing. . Fourth, Microsoft released the new model of the Bank of China in the fourth quarter. In 2017, the number of users of Baidu Post Bar, a single popular console game, exceeded 1 million, reflecting the high development potential of console games in the Chinese market. In 2017, the proportion of China's popular new console games in the open country is still very low, prompting a considerable number of players to consume through overseas servers, but the quality games in the country still have outstanding market performance. The main characteristics of domestic home game consoles are: First, domestic home game consoles perform well in home entertainment scenes, occupying a major market share in the low-end market; second, domestic high-end home game consoles will enter a period of rapid development, domestic Manufacturers actively tried to develop high-quality console games. Third, domestic game consoles with multiple functions such as video, VR, and family interaction were welcomed by the market. (five) VR games In 2017, VR games achieved a total sales revenue of approximately 400 million yuan, an increase of 28.2% year-on-year; more than 800 popular VR games, the market has high differentiation of high-end and low-end products. The main features of the VR game market are: First, the lower quality domestically produced VR games have had a negative impact on the market. The practitioners have taken initiatives to increase the VR game threshold and increase market confidence. In recent years, the quality of domestic VR games has been mixed, affecting the experience of VR games. Nvidia, which masters the core technology of VR graphics processors, has released VR FunHouse, a game that reflects VR's cutting-edge technologies. The free game is expected to become a benchmark in the industry, effectively raising the technical threshold of VR games and boosting the overall quality of Chinese VR games. Second, the market competitiveness of domestic VR game equipment continues to increase. With the upgrading of domestic VR enterprise technology, the market share and recognition of domestic VR game devices have also continued to increase. For example, domestically-owned brand TCL's VISION VR and 360-degree panoramic VR camera Alcatel 360, sales have ranked fifth in the global VR market share; ants view second-generation VR uses inside-out cutting-edge positioning technology, and its infrared controller can accurately Identifying the edge of the user's finger, the technology is ahead of the same price, and it is also widely recognized by the market. Thirdly, VR game devices have become more differentiated, and the quality of imported high-end VR game devices has been recognized by domestic core players. Non-core gamers prefer domestic VR devices that take into account both VR video and VR game functions. In terms of VR game content, the immersive experience of VR games is stronger, and the scene experience classification becomes a unique subdivision of such games. According to domestic mainstream VR application platform data, VR games are focused on shooting, adventure, and leisure, with the proportions of 16%, 14%, and 14%, respectively. Due to technical limitations, shooting and casual games are easier to implement in the R&D aspect than in the action games, and the game experience of players is even greater. In terms of VR game equipment, in 2017, high-end VR hardware products are mainly imported products such as HTC VIVE, Oculus, PS VR, Gear VR, etc. High-end VR hardware products are mainly made by domestic equipment, such as Storm Mirror 5, Huawei VR , millet VR glasses, big friends M2 one machine. China's best-selling products in the VR consumer market are still dominated by medium and low-end and multi-functional VR glasses. The price differentiation between products of different grades is relatively large, reflecting that the market still has great enthusiasm for VR devices and the market consumption potential remains to be developed. In addition, sales of high-end equipment increased compared to 2016. In 2017, the popular VR games in the Chinese market are still dominated by foreign players. The client VR game distribution platform is mainly for the Sony PS platform and Steam. The adaptation devices are mainly PS VR, HTC Vive and Oculus. The mobile VR game is based on the Android platform. Mainly, adapter equipment is broader. Third, the development characteristics of the game industry in 2017 In 2017, the Chinese game market has the following characteristics: First, the game user stock market has formed and new users have been reduced. The mobile game market has driven the overall market revenue to continue to grow steadily, thus driving the annual revenue of online games to exceed the 200 billion yuan mark. Secondly, the main players in market competition have achieved the survival of the fittest, the market has returned to rationality, and top ranked online game product R&D and operating companies have occupied a major share of the market, and the SMEs' startup costs and survival costs have increased. Third, quality online games are constantly emerging, and IP plays a significant role in the process of online game quality. The use of IP also returns to rationality. Fourth, the electric competition continues to be hot, especially the "League of Legends" finals and the "King of the glory" mobile game events held to promote the e-sports industry chain to improve and mature. Fifthly, the transformation and upgrading of the game and entertainment industry promoted by the Ministry of Culture has promoted the healthy development of the game and entertainment industry, and has greatly promoted the rapid development of the upstream and downstream of the traditional game and entertainment industry towards competitive and large-scale development. It has become a game industry that cannot be ignored. An emerging force. Sixth, the pace of going out is increasing. With the increase in the quality of Chinese games, especially mobile game products, in addition to the original Southeast Asian market, Chinese online game companies have successively seized the markets of West Asia, Africa, and Europe and the United States. Seventh, the industry policy is further improved. The “Notice of the Ministry of Culture on Regulating Post-regulation Supervision of Online Games Operations†was formally implemented, which clarified the operating norms of the online game industry and was conducive to building a positive industry ecology and protecting the legitimate rights and interests of consumers. Eighth, the market order is further standardized, and the Ministry of Culture organizes and conducts three special investigations. To carry out illegal and illegal online games to “review†investigations and deployments, deploy comprehensive enforcement agencies for cultural markets in Beijing, Shanghai, Hubei, Sichuan and other places, and investigate and punish 12 online game operation companies; rigorous investigations include the promotion of obscenity, pornography, gambling, violence, and harm to society. Public cultural banned internet cultural products such as Gongde, supervising the comprehensive law enforcement agencies of cultural markets in Beijing, Shanxi, Jilin, Jiangsu and other places, investigating and punishing 23 Internet cultural business units; strictly checking online games to promote and banned contents containing harmful social morality and regulating online games Product promotion and promotion activities, supervising the implementation of comprehensive law enforcement agencies in cultural markets in Beijing, Shanghai, Jiangxi, Guangdong, and Sichuan, and investigating six online game operation companies. Fourth, the development trend of China's game industry First, the market scale will continue to grow. With the maturity of the mobile game market and the upgrading of game users' consumption concepts, the online game market still has great growth potential. Second, the effective guidance of the government and the upgrading of consumer spending will continue to promote research and development of quality games with content, content, and innovation. Third, the maturity of mobile games and e-sports will promote the development of mobile e-sports in China. Mobile e-sports will gradually develop in the direction of specialization, commercialization, and professionalism. Fourthly, the game has become an important form of overseas export of Chinese culture, and more Chinese game companies will participate in the competition in overseas markets. Fifth, in terms of industry policies, industry authorities will further regulate market operations, protect user rights and interests, and encourage young people to innovate and create original products. YUOTO Vape,YUOTO Disposable Vape,YUOTO Vape Kit,YUOTO Vape Pod tsvape , https://www.tsvaping.com