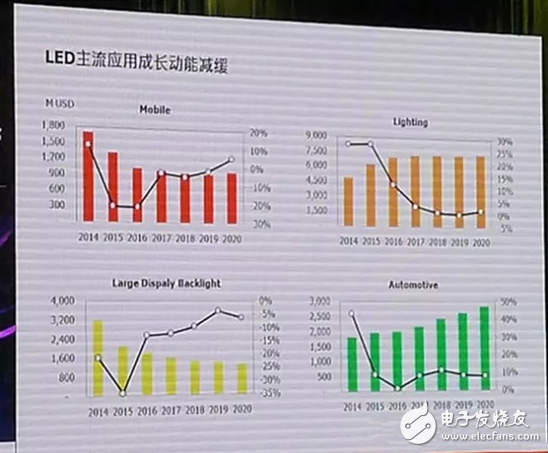

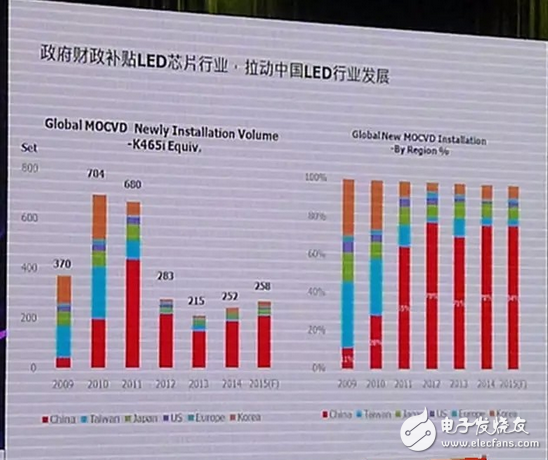

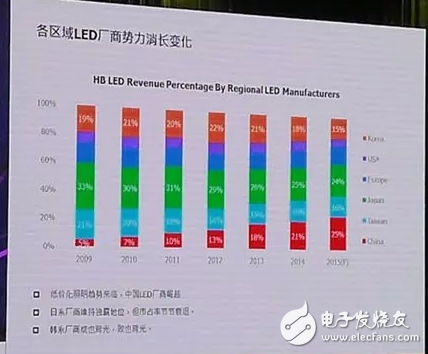

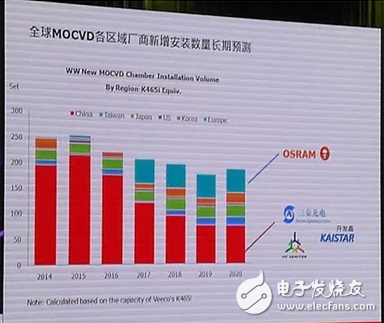

According to forecasts, the global high-brightness LED market in 2015 reached 14.52 billion US dollars, but the annual growth rate was only 2%. Although the number of LEDs continues to grow under the demand of lighting, with the increase in efficiency, the number of LEDs used is reduced, and the price pressure is reduced. Therefore, it is expected that the annual compound growth rate of the LED industry will be difficult to reproduce the past 10% in the next five years. The above growth rate, industry growth will slow down. Earlier, senior industry analyst Chu Yuchao described his supply and demand outlook for the LED industry in 2016 at an LED lighting market analysis meeting. The growth rate of output value has declined significantly in recent years. In reviewing the past LED market, Chu Yu pointed out that in the past decade or so, it has shown a high growth trend. First, before 2007, LED applications in the backlight and keyboard backlight of mobile phones led to an increase in market demand. Since 2009, TV backlights have been introduced into the application, and then the take-off of the smartphone, tablet, and LED lighting markets, the output value of the LED market has been pushed up with a wave of new applications. The study found that over the past decade or so, the average annual compound growth rate of the entire industry is about 20%-30%, but in the past two years, the growth rate of output value has shown a downward trend. Growth momentum of various mainstream applications slows down He said that according to relevant statistics in 2015, the growth of output value this year is probably maintained at 2%. Even once it was suspected that this year will show a negative recession. The main reason is that the growth momentum of various mainstream applications has slowed down. With the reduction in the number of uses and the increase in efficiency, the output value has gradually declined. Although the lighting and car parts continue to grow, the growth has slowed down. The part of the car is because it takes a long time to introduce, but the growth rate is not as obvious as the previous backlight. Therefore, it is estimated that the annual compound growth rate of the entire industry from 2015 to 2020 is only about 3%. Most manufacturers turn into niche markets At the same time, as the price of mainstream applications falls, it will also make the whole market appear a relatively smooth state. In the case of seeing the backlight market price is too low, most manufacturers are moving into niche-type markets such as UVI. In the case of many vendors investing resources, there may be some technological breakthroughs and room for growth in these niche-type markets in the future. Industry supply and demand balance is solved by supply side From an optimistic point of view, in the next few years, a large number of manufacturers will be reshuffled by the survival of the fittest, and the trend of falling prices will slow down, making the industry's compound annual growth rate even reach 10%. From a conservative perspective, it is that other niche markets have not been brought up, including the technology has not been broken, or the demand side has not been opened. In this conservative situation, the growth of the industry may even appear as a negative recession. Looking to the future, the growth of the LED industry has come to a mature stage. Demand has been presented in a smooth and stable state, and the balance of supply and demand in the entire industry can only be solved by the supply side. Financial subsidies drive the development of the press station day When talking about the supply side, Chu Yuhao said that he would talk about MOCVD. According to reports, the number of MOCVD conversions for the K465i model in 2015 was about 258, of which there were almost 200 in China, accounting for 80%. Despite the sluggish industry, Chinese manufacturers continue to expand. Since 2010, due to the local government's financial subsidies, China has developed rapidly in the entire chip industry, which has led to LED packaging throughout China, and the downstream application industry has continuously improved its position in the world. Comparing the output value of LED packaging manufacturers in various regional markets of China's LEDs, it will be found that before 2009, the share of Chinese LED manufacturers in the whole market is very small, probably less than 5%, but by 2015 it has reached a quarter. It shows a growing trend, and it has squeezed the manufacturers in Taiwan and the market share of Japanese manufacturers. South Korean manufacturers succeed in the backlight market The situation of Korean manufacturers is relatively special. It is understood that the share of the whole market was less than 15% before 2009. After 2009 and 2010, with the rise of backlight applications, many manufacturers once climbed the dominance of the world's second. . However, in recent years, especially this year's recession is very large, with a global market share of only 15%. It can be seen that Korean manufacturers can be said that "there is also a backlight, and the backlight is also backlit." Global LED manufacturers adjust their strategies accordingly According to the changes in these forces, we have seen strategic adjustments in various LED manufacturers around the world, including or adopting a downsizing strategy (Samsung, LG innotek), or taking a split sale (Lumileds), or seeking to reposition ( Osram), Chinese manufacturers have continued to expand (Sanan Optoelectronics, Dehao Runda) in order to achieve a leading position in the market. Observing the different development status of manufacturers in various regions, Korean manufacturers including Samsung and LG innotek are currently downsizing. According to statistics, in 2015, the application of Korean manufacturers' large-size backlights and mobile phone backlights increased by nearly 70%. Therefore, when the backlight market declines, Korean manufacturers will bear the brunt. Although Korean manufacturers are also trying to increase the proportion of automotive lighting, they can only grab some market share through Hyundai's supply chain. As for the lighting market, the part is even worse. Basically, it has been beaten by the low-cost strategy of Chinese manufacturers. Looking for a new application market to reduce the scale of winter It can be seen that the Korean manufacturers including Samsung and LG have had a hard time. As early as September 2015, Samsung downgraded the LED business unit to an operation group, and LG took a new treatment for its LED business (LG innotek), and sold the sapphire wafer business under LG Iinnotek to SSLM. . The Rijin Group is currently liquidating its LED chip and packaging companies and has applied for a reorganization process on December 18. The first-line manufacturers are like this, let alone the second-tier manufacturers who have some "relative" relationships with Samsung and LG Group. In fact, when Samsung and LG are in a state of “not eating enoughâ€, it is difficult to throw excess backlight orders to second-tier manufacturers. So it would be surprising that LG Group would end the LED business. South Korean manufacturers will also have to find ways to seek a newer application market, or to reduce the scale to support the downturn. Repositioning and cutting into the general market to kill Although some of the manufacturers are shrinking, OSRAM has announced an investment of 1 billion euros in a new 6-inch sapphire substrate-based LED chip factory in Kulim, Malaysia (with a total investment of 1 billion euros in 2016-2020). Since the investment case includes the chip process from the previous LEDepi to the latter stage, it is assumed that if the equipment is fully in place, it will have more than 200 MOCVD capacity (K465i Equiv), and the monthly number of films will reach TIE 800,000. More than one piece. More importantly, however, Osram's huge capacity is basically directed at general lighting. Chu Yuchao believes that Osram and China are killing in the general lighting market, which is a strategy that has to be done. He analyzed, because the Osram Group's current operating share is divided into four parts, one is Opto Semiconductors, including some components; the second is Lamps, including traditional bulbs and LED bulbs; the third is Special LinghTIng, such as vehicles Lighting products; finally LighTIngSoluTIon&Systems, including some control system products. Today, Osram has spun off the unprofitable bulb business and sold it to Chinese manufacturers to refocus on Opto components and system control. However, most of the business of OSRAM Opto components is in the leading position of automotive lighting. If the whole business is put on the car lighting in the next ten years, its growth rate can only increase with the increase of industrial penetration. Natural growth, it is difficult to have a big increase, so it has to cut into general lighting, so it is necessary to compete fiercely with other competitors in the market. Jinshajiang's acquisition of Lumileds has a high failure rate Previously, the European lighting giant Royal Philips planned to cut LED and automotive lighting business Lumileds and sold 80% of the shares to China's Jinshajiang Group. However, this acquisition is currently blocked by the US Overseas Investment Committee's defense security concerns. . However, Chu Yuchao believes that this has little to do with national security issues, but the impact of political issues is greater. In his view, the probability of this acquisition failing in the future is high. First, it will be affected by political factors. In addition, this year is in the US presidential election. It is estimated that before the election, the US government will avoid some extra-budgets. Make a decision. Therefore, Lumileds finally has to wait for a long time to observe. In the future, increase the value-added innovation application of products Looking at the strategic changes of Chinese manufacturers, the Chinese government has spared no effort in supporting the LED industry in the past decade, including through various financial subsidies, or various demonstration projects and projects to drive the entire LED industry. However, the results of the past decade have not been as good as ideal. First of all, at present, in the case of a large amount of subsidies, the industry has over-invested and the waste of resources has caused overcapacity, which has caused a serious imbalance between market supply and demand. In addition, the industrial structure is also seriously unbalanced and needs to be adjusted. Most enterprises can directly put into production as long as they purchase equipment. In fact, most of the raw materials of the most upstream equipment are still dependent on foreign imports. Therefore, this does not help the improvement of the whole industry. Chu Yuchao predicts that the future direction may be to increase the added value of products and increase the application of innovation, including emphasizing technological innovation and optimizing the industrial structure. China’s large-scale subsidies may no longer exist Chu Yuchao pointed out that as a key area of ​​concern for China's "13th Five-Year Plan" and "Made in China 2025" programs, wide-bandgap power semiconductors are a "significant learning", and most manufacturers have the opportunity to get subsidies as long as they are close to semiconductors. Now, it seems that more and more manufacturers are starting to move closer to semiconductors. Therefore, he believes that large-scale subsidies will no longer exist in the future, but at the same time he also acknowledges that there are policies and countermeasures. Huacan Optoelectronics recently announced that it will invest RMB 6 billion in Zhejiang Yiwu to build a large LED base. He said that due to the completion of some subsidies for the Xiamen Municipal Government, including Sanan Optoelectronics, the development of Jingjing continued to have a plan to expand production. Later, it was necessary to see that the expansion capacity of Huacan Optoelectronics could not be implemented, and the new plant of OSRAM is also expected. It will be completed and put into operation at the end of 2016 and at the beginning of 2017, and it will also have a certain degree of impact and impact on the industry. In addition, once some niche-type applications gain technological breakthroughs, it will also enable manufacturers to order MOCVD machines to expand production capacity, which will have a certain impact on the future of the industry. Global LED industry supply and demand will continue to be imbalanced According to statistics, in 2015, the number of LED wafers produced by the global LED wafers reached 713 million. Looking forward to 2020, the number of LED wafers will reach 100 million or more. The growth rate is 9%. The expansion of the European manufacturer Osram has also brought the industrial supply to the next level in 2017-2020. Chu Yuchao said that with the sharp increase in lighting demand in 2014, the demand of the entire industry has grown, but because of the strong demand from customers in 2015, many LED chip manufacturers have to shorten the chip size and increase the brightness to reduce The cost, as the number of LEDs used is reduced, or the chip size is reduced, so that the number of LED Epi wafers is reduced. Looking forward to 2016 to 2020, the overall LED market demand continues to grow, but the continued expansion of the first-tier manufacturers has caused the LED industry to continue to be oversupplied. In the case of each manufacturer's expansion, there is still a large gap in the supply and demand gap. He pointed out that these are just the supply and demand gaps in the name. For the first-tier manufacturers, these gaps in supply and demand do not persist. Because the current price is too low, the requirements of customer specifications are very high. Therefore, only the first-tier manufacturers have the ability to obtain orders, and the second-tier manufacturers simply do not have the ability to obtain orders, so they can see that some first-tier manufacturers are in full. Under the circumstance, the production continues to expand. The exit mechanism led to the trend of the meager profit era At the same time, he also said that in view of the current development prospects of the industry, the era of low profit has become an inevitable trend. The main reason is that there is a problem with the exit mechanism. For many LED manufacturers, especially the chip factory, the proportion of depreciation in its entire operating cost is about 20%, which is not high. In particular, many manufacturers still have no financial equipment through financial subsidies. Depreciation problem. Therefore, many manufacturers will choose to continue production as long as their prices have reached the variable cost. So you can see that many manufacturers retreat when the price is too low and the market is not good. When the market is good, they will start to come back to production. This continuous repetition will affect the prospects for improvement in the supply and demand of the entire industry. in conclusion Finally, Yu Chao has reached several conclusions. He believes that looking back at the poor demand in 2015, the large reason is the exchange rate fluctuations, resulting in a decline in demand in the end market, and the client requirements to reduce costs. However, by 2016, the global economic situation has slowed down, the United States has begun to enter the recovery phase, and other regions such as Europe and Japan continue to stimulate the economy through QE policies. Although the client continues to demand price cuts, the decline is not expected to be as exaggerated as it was last year, so the entire 2016 demand seems to be a relatively smooth phase. In the medium and long-term outlook, the meager profit era is the norm. How to end the entire meager profit era depends on the development of the exit mechanism of this market, but Chu Yuchao said that in fact, this wave of the LED industry is a crisis and a turning point. In the past, various manufacturers still had a certain degree of illusion about the LED industry. When the LED lighting market came, the business opportunities for this wave of demand were very large, and each manufacturer could have a certain living space in the big market, but when When the LED lighting market really came, it found that it was difficult to make money, so many manufacturers would think about exit and transition strategies. For European, American, Japanese and Korean manufacturers will think about how to withdraw from this market. He said, "For all manufacturers, this is both a crisis and a rare opportunity in the past 100 years, that is, how to find a position of their own through overseas purchase and repositioning in the market."

Three-axis Smartphone Stabilizer is composed of pan axis, rolling axis and tilt-axis. With a gyro-stabilized gimbal system, it keeps stabilized or steerable horizon with automatic calibration to give you an unprecedented smooth shooting experience.

Three-Axis Smartphone Stabilizer is born for video lovers. it stabilizers the video footage horizontally, without sacrificing the thrill of dynamic motion in the video.

Wewow focusing on handheld stabilizer is a technology company which does R & D independently. With Wenpod series product released, the company achieved the industry's praise and quickly became the leader of the smart stabilizer industry.

Our service

1. Reply to you within 24 hours.

2. Already sample: within 1-2days.

3. Shipping date: within 24 hours once get the payment.

4. 12 months warranty.

5. After-sales service, solve within 3 working dates.

If you have any questions, please contact with us directly.

Wewow appreciates domestic and international business relationship!

Three-axis Smartphone Stabilizer Three-Axis Smartphone Stabilizer,3 Axis Handheld Gimbal For Smartphone,Smartphone Gimbal For Cell Phone,Three-Axis Stabilizer For Smartphone GUANGZHOU WEWOW ELECTRONIC CO., LTD. , https://www.stabilizers.pl