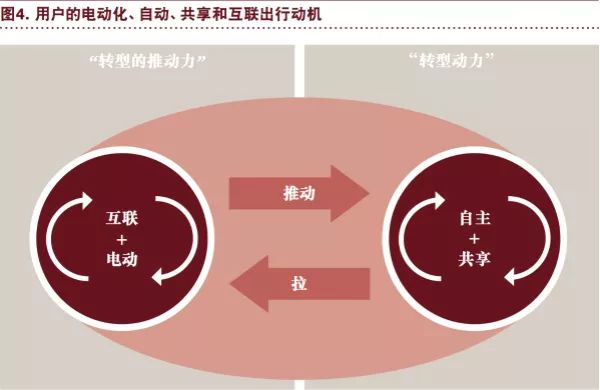

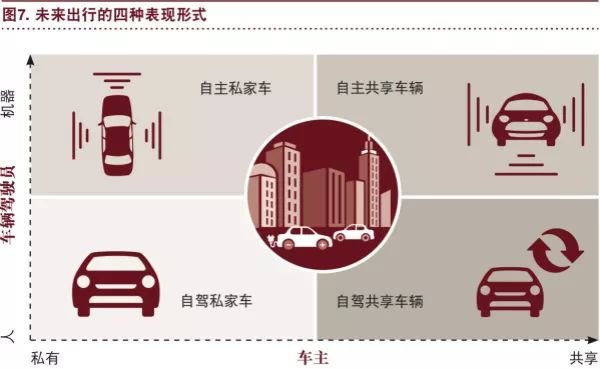

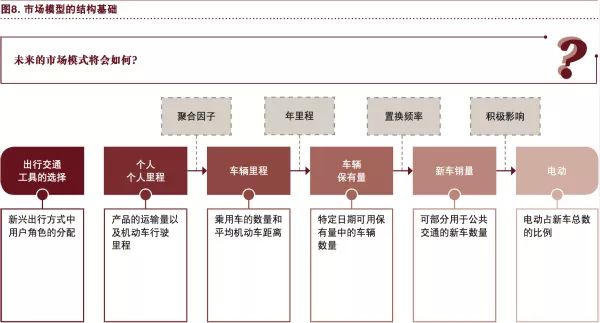

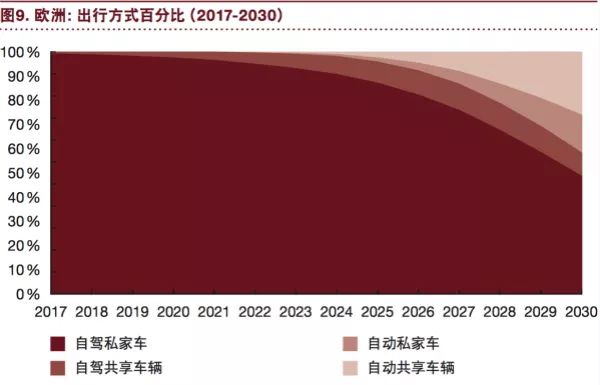

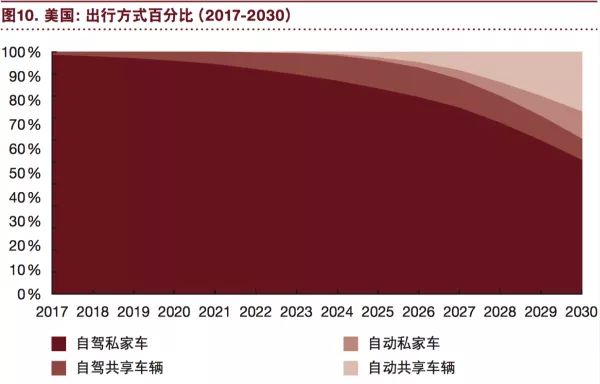

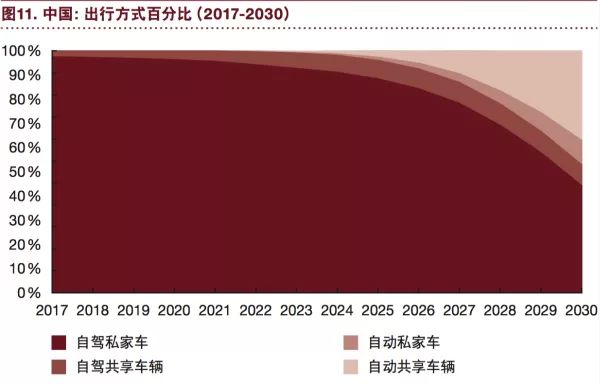

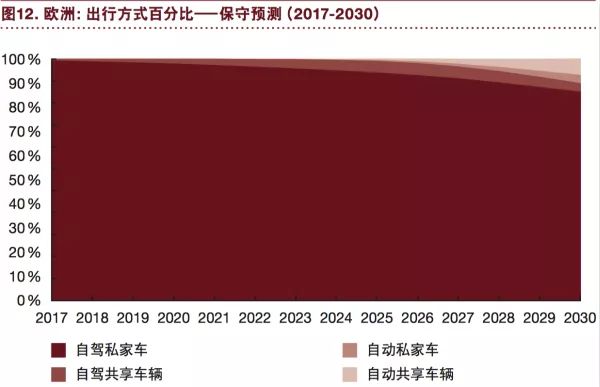

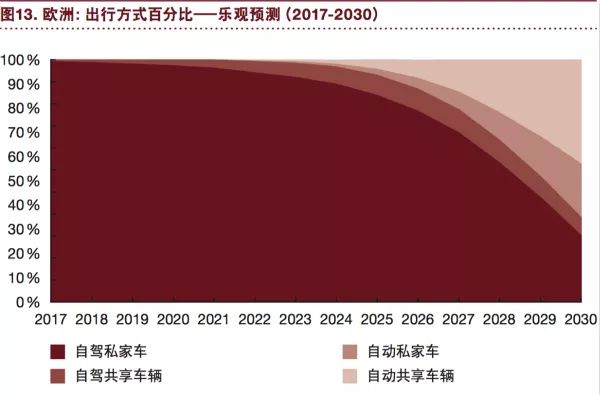

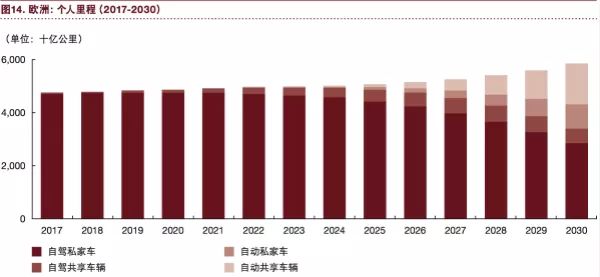

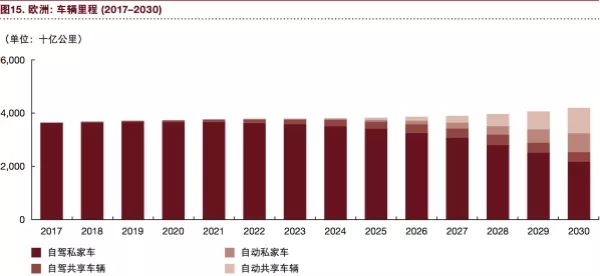

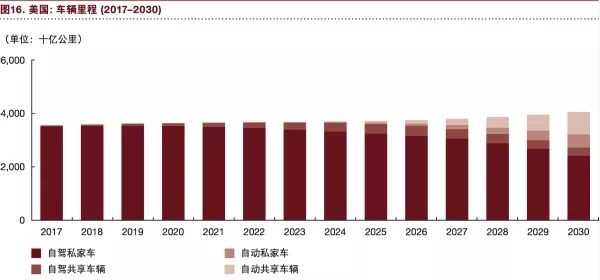

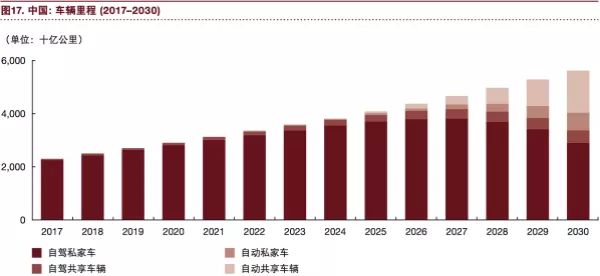

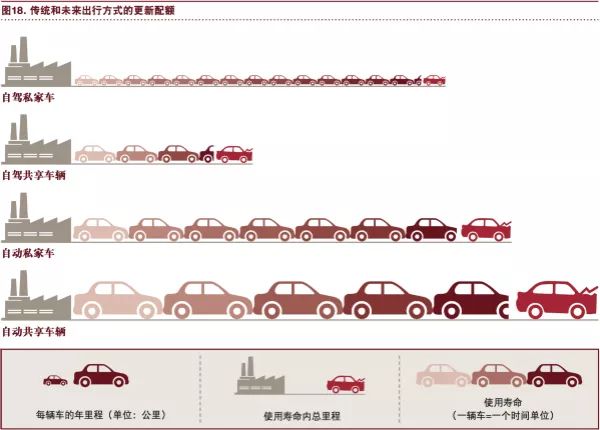

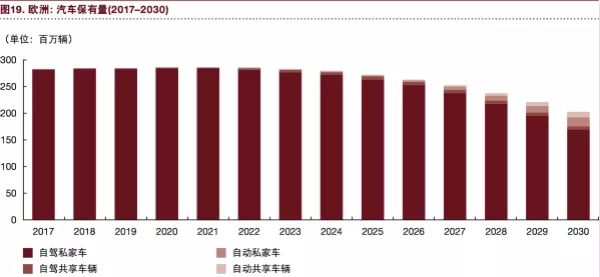

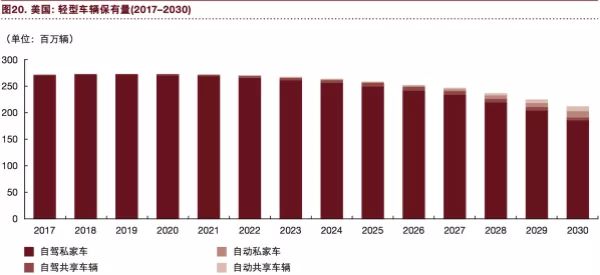

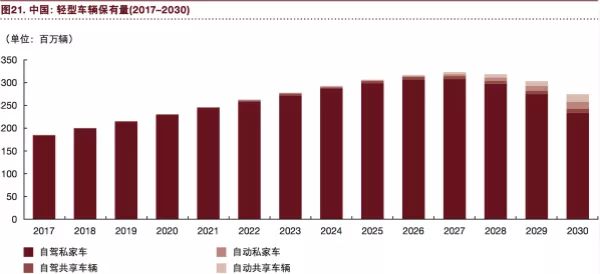

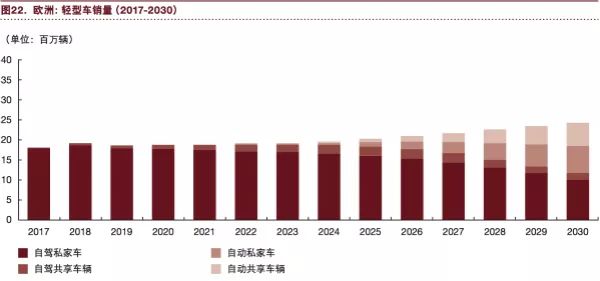

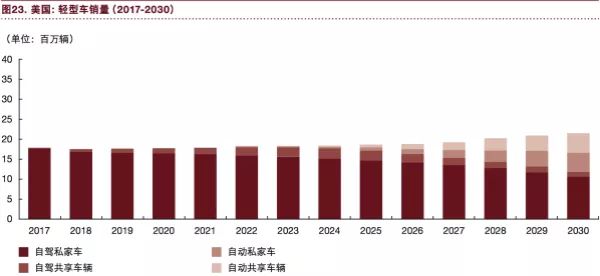

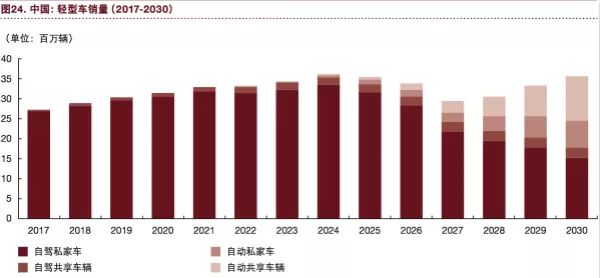

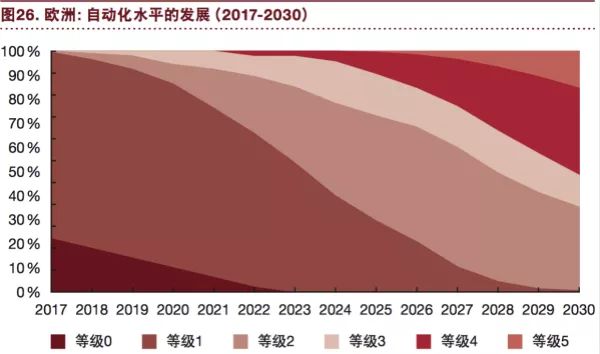

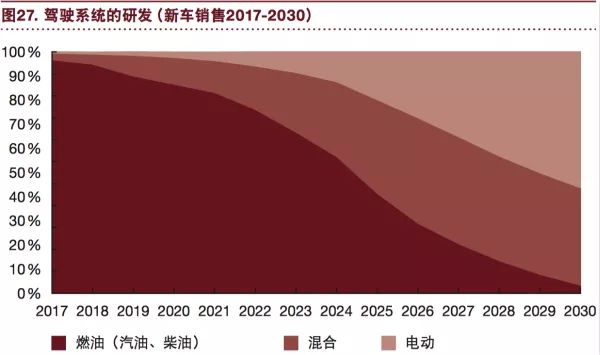

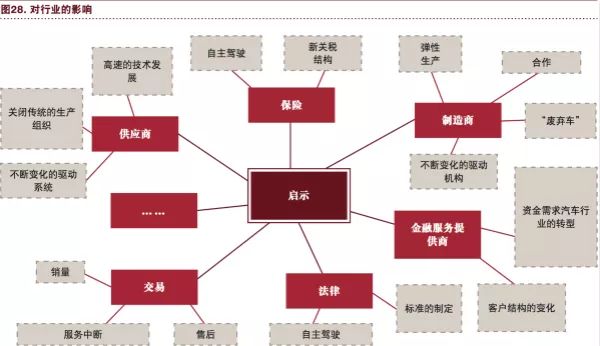

Cars have long since transformed from a technical commodity into a social commodity: we can ensure our personal travel and social participation, shape our cities and landscapes, and build our time and space thinking structure. At present, the automotive industry is facing unprecedented changes that will have a profound impact on the industry and users. This is an in-depth report from PricewaterhouseCoopers. Since the advent of smart phones, if a certain technology can improve the ease of consumer life, even if it is very complicated and expensive, it cannot stop the enthusiasm of customers. In other words, users value convenience and simplicity. These core values ​​make the car the most typical technical and cultural project of the 20th century. It is time to incorporate these attributes into the technical and social context of today and tomorrow. The automotive industry has the opportunity to shape this fundamental restructuring process. When formulating strategies and business models, companies should not only consider direct product buyers, but should include all users and groups affected by transportation issues. Cars have long since transformed from a technical commodity into a social commodity: we can ensure our personal travel and social participation, shape our cities and landscapes, and build our time and space thinking structure. So what will happen in the future? The automotive industry will fully realize eascy The car of the future will be electric, automatic, shared, interconnected and updated year after year, in short, “eascyâ€. Because of the electrification, exhaust gas and noise emitted into the environment will be reduced. Because it is automatic, personal time and space can be saved. Users no longer need a driver's license, so the scope of application is broader. Because it is no longer necessary to buy directly, but it is purchased in batches, it is cheaper. The automotive industry is facing unprecedented changes that will have a profound impact on the industry and users. Therefore, this article will predict the basic restructuring of the automotive industry in terms of time, capacity, and complexity. Based on the research results, this paper will analyze what kind of changes the user's travel behavior will produce, and what kind of impact it will bring. Before a detailed analysis, we must first understand the precise meaning of electric, automatic, shared, interconnected, and yearly updates: Electric: If there is no electrification of the drive mechanism, then zero emissions from personal traffic are almost impossible to achieve. First, there is the problem with local components - cars now emit only ultra-low levels of harmful substances, dust and noise. Moreover, "zero emissions" seems to be a global initiative: the electricity used to recharge vehicles will come from renewable sources of energy to ensure carbon-neutral travel. Automated: Rapid advances in areas such as artificial intelligence, machine learning, and deep neural networks make it possible that the recent seemingly utopian utopia is no longer possible - that is, the development of autonomous vehicles, without manual intervention even under complex traffic conditions. This will completely subvert the application of personal mobility platform. Just a few years ago still unimaginable application scenarios have emerged one after another. Sharing: In recent years, many large cities have built carpool facilities. Although these are usually pilot projects or civic programs at present, the concept of sharing will gradually become economically viable with the introduction of automatic vehicles. We will no longer need to search for shared vehicles in the surrounding areas: simply book vehicles with convenient "on demand" services, no matter where you are. Interconnection: The fourth dimension of "eascy" is the networking of vehicles and the outside world, called the concept of "connected cars." This term actually involves two concepts. On the one hand, it applies to Car2Car and Car2X communications, ie the networking between vehicles and other vehicles or traffic infrastructure such as traffic lights. On the other hand, the term also covers the networking of passengers in the car with the outside world. In the future, passengers will be able to communicate, work, access the Internet or use multimedia services while the vehicle is in motion. Year by year: Development themes such as electrics, automation, interconnection and sharing will promote a significant increase in the speed of innovation in the automotive industry. The five to eight year model cycle that has been common in the industry may soon become a thing of the past. Instead, the range of models will be updated year by year to integrate the latest hardware and software development results. Naturally, due to the high cost of purchase, customers do not want to buy a new car every year, so the shortened innovation cycle will mainly come into the market by regularly updating shared vehicles. From the user's point of view, these five dimensions can bring a wide range of benefits. All forecasts show that the ease of driving, safety, economical applicability and comfort of vehicles are all significantly improved. At the same time, changes in individual travel solutions will prompt the automotive industry to further implement transformations. The focus is on existing car ownership and new car sales. Ultimately, these two variables determine the value chain of automotive production and are therefore of equal importance to the future business model of manufacturers and suppliers. In the study will focus on the world's three largest automotive markets, namely Europe, the United States and China. This study starts from the user and builds a model of future market development. The repositioning of the industry can be described by three external factors, three modeling results, and three meanings. external factors Our travel habits will change: our travel behavior will be completely changed. Once the legal issues are clarified and resolved, and major technical obstacles are overcome, the sharing and automatic proportion of overall road traffic will increase substantially. We predict that by 2030, more than one-third of miles will already involve sharing concepts. At the same time, user behavior will be increasingly closer to automatic travel. In this respect, the PricewaterhouseCoopers Autofacts calculated the mileage by 2030, which may even increase to 40%. It is expected that the speed of development in Europe and the United States will be roughly parallel. In contrast, China's penetration of shared and automatic travel will exceed the Western world. This may make China a leading country in the transformation of the automotive industry. More people’s travel mileage will be extended: As the population data grows and travel demand increases, vehicle mileage will continue to increase. At the same time, taking into account the ease of driving, safety, and economic suitability of vehicles, the overall travel trend will develop in the direction of individual travel. In addition, personal transportation may be an excellent solution for people who have not had a chance to travel in the past, for example, people with disabilities. The last factor is that the number of miles may increase due to the fact that the parking space may not be full due to automatic vehicles. Therefore, PwC Autofacts predicts that by 2030, personal mileage in Europe is estimated to increase by 23% to 5.88 trillion kilometers. The United States is forecast to achieve 24% growth, while China reaches 183%. The strength of the use of automobiles in the future will be significantly increased: future automatism, especially shared automotive vehicles, will achieve significant improvements in capacity compared to current conventional vehicles. Therefore, the annual mileage will increase significantly. As a result, the vehicle replacement rate will increase significantly, although its effective life mileage will increase. The assumption that the vehicle's life mileage will increase in the future will be closely related to the advantages of automatic and interconnected driving that will lead to an accident reduction. The cost of maintenance and repair will decrease, and the reduction in the accident rate will also mean that the number of miles that the vehicle can travel will increase significantly. Modeling results Car ownership in some markets will fall sharply: According to the increase in fleet utilization, the number of vehicles needed in the future will decline. PwC Autofacts predicts that by 2030, European car ownership will be reduced from the current 280 million vehicles to about 200 million vehicles, a reduction of more than 25%. We expect the U.S. car ownership to decrease to 212 million vehicles, a 22% decrease. Due to the different market conditions in China, although the utilization rate has increased, its holdings may increase by nearly 50% over the same period to reach 276 million vehicles. Car sales will continue to rise: In spite of declining occupancy, car sales will increase significantly. Traditional vehicles will stay in the possession for a long time. In contrast, automatism, especially shared automotive vehicles, will change frequently, leading to increased sales. During the transition period, new car sales across Europe will increase by 34%, from approximately 18 million to more than 24 million. PwC Autofacts predicts that by 2030, new car sales in the United States will reach approximately 22 million vehicles, an increase of 20%. For China, sales are forecast to reach 35 million vehicles, an increase of more than 30%. Autopilot and electrification complement each other: driving autonomy (so-called autopilot) will initially be limited to a few narrowly geographically restricted areas, most likely inland cities and highways. This is because the two dimensions of automatism and electrification complement each other. For example, a self-driving vehicle expressly requires the use of electric driving because the "inland cities" use case is usually only for this scenario. One example is the automatic charging process using inductive charging. The mutual influence of these two dimensions can achieve a positive overall effect. Therefore, by 2030, in the EU's new car sales, the pure internal combustion engine will probably have a small single-digit share. In this scenario, more than 55% of new cars will be fully electric. 40% of new cars will still use hybrid drive technology combined with internal combustion engines. Enlightenment Rapid redistribution of R&D investment: It is already evident that the automotive industry will begin to compress its product range. In the framework of "Global Innovation 1000", PricewaterhouseCoopers calculated that by 2020, investment in this field will drop by 19%. However, this is not necessarily a bad sign. The overall conclusion of the study concludes that companies that invested R&D budgets in software solutions rather than products have shown stronger growth than other competitors. The figure also shows the direction that manufacturers and suppliers need to take. With the exception of Tesla, none of the automotive industry has yet reached the top 10 of the most innovative companies in the world (though there are only five companies ranked between 11 and 20), although the highest R&D expenditure is for a German car manufacturer. Overall, R&D expenditures in the automotive industry fell by 4% between 2015 and 2016. The most significant feature of this period was digital innovation and transformation. Between 2020 and 2025, the long-term development structure will be determined: especially between 2020 and 2025, manufacturers and suppliers will have to invest heavily in customer-centric innovation while coping with falling profits. Traditional automakers will have to consider how much capital they are prepared to invest in their service providers to offset the potential reduction in their core business. At the same time, the increase in sales of new vehicles also requires manufacturers to add additional “hardware†capacity investment, and companies that implement the flexible and scalable concept will be able to play an active role and lead the future development of the industry after 2025. The future business model covers car sales and operations: In the future, focusing only on car production and sales will not be enough. Manufacturers and suppliers need to rethink their business model to manage the five dimensions of the “eascy†model. Factory delivery will no longer be the last link in the automotive value chain, and the value chain will extend to all types of use throughout the vehicle's life cycle until the vehicle is finally recycled. The automotive industry's customers and target groups will no longer be limited to the direct buyers of vehicles, but will cover all product users, private and shared usage models. The direct software-based interaction with each customer supported by the brand experience will further extend the benefits beyond the life cycle of the customer relationship. Focus on the user Different travel use: If manufacturers and suppliers further expand their business model to cover the “operational†elements, the traditional target data of the industry, namely the importance of car sales and car ownership will be weakened. Even so, it is important for companies to understand how these two kinds of data will change in the coming years. Therefore, the first model to quantify the five “eascy†dimensions in the mathematical model developed by PricewaterhouseCoopers will begin with the user (“roleâ€). By modeling the behavior of the user, personal mileage can be calculated to calculate the entire vehicle mileage in a particular market. On this basis, greater certainty will be achieved when predicting car ownership and car sales. To model the usage preferences within the market under review, we identified three different categories. The "role" is mainly based on people's attitudes and acceptance of various forms of travel, and the way they use them. In this process, some major regional and cultural differences must be considered. Other features within the user community include the age structure and its living environment—urban or rural environments. This sort of logic allows us to consider the changes in the proportion of the population of each user group over time. Trends from 2017 to 2030: The young generation with a technical mindset will play a key role in promoting the development of sustainable and convenient travel solutions in the coming years, and will also show the attitude and behavior of successive generations. In contrast, middle-aged people tend to have a certain degree of skepticism in regard to the development of new travel plans, at least at the beginning. However, in terms of a more modern-oriented role, the proportion of the population will inevitably shift – not only in Europe and the United States, but also in China. And in China, this process may come more quickly and with greater intensity. Here, technological change can get the best cultural and political soil. By 2030, the proportion of the population of “traditional†users in China will drop significantly. Self-driving electric taxis and extensive electrified public transport will play a major role in this transition. In terms of technological development, China's urban areas may catch up with the United States and Europe in 2030 and may even surpass it. The level of air pollution in various cities in China will be a factor in the introduction of carpooling and ride-sharing services in urban layout in the next few years, which together with street congestion will constitute two major driving forces. These services may soon be seen as alternatives to traditional travel forms. What is the status of future travel? Who will travel and how to travel? Travel needs and preferences are constantly changing: Changes in “role†mean that travel needs will change in the coming years. Various "eascy" dimensions have their own drivers. For example, the main driver for autonomous driving is time saving and safety. The primary driver for sharing is cost. Interconnection and electrification can be seen as a healthy factor in the transformation of the automotive industry. After all, the market penetration of electric vehicles is not initially driven by the demand structure of the market economy, but is mainly a political and regulatory issue. "Yearly Update" attributed to the high-speed innovation of other dimensions of "eascy", especially in the fields of "automation" and "electricalization", the basic technologies in these fields are rapidly improving and therefore cannot be integrated into the traditional model cycle. The “model year†should not increase such facade activities, and the auto industry must use the latest technology to launch “model cars of the yearâ€. In some cases, these technologies also include retrofitting early model cars of the year to promote their replacement. Use instead of owning: Changes in behavior will define future travel patterns. The breadth and depth of travel options will increase significantly. This point has been demonstrated in the increase in the number of providers mentioned in this section. New startups are competing with existing car, transportation and logistics companies for market share. There are two different forms of expression for the shared travel mode: time-sharing of cars and online bookings. Time-sharing car vs network car: Time-sharing car has two manifestations, namely site-style and free-stop. The basic difference between these two forms is the availability of vehicles. The site-based time-shared rental car model means that vehicles can only be called from pre-defined stations, and the free-standing selectable area reflects the provider's entire business scope. In contrast, online booking is only about trip sharing. This concept is becoming more and more popular and can no longer be considered marginal. By 2017, the number of global users is expected to increase to 338 million. In general, there are three different trends: Online Time-To-Day Rental of Car Dealers to Create Driving Community The online platform will serve as a broker to provide journey services for private car drivers Taxi company providing services through the application The user wants to use a self-driving car: What is the relationship between the time-of-rental of a car and the automation dimension, that is, automated driving? In order to be able to standardize the level of automation, Germany has introduced phase 0 to 5 models at the national and international levels. There are different levels of automation: this is a constant public debate. For example, in a particular geographic area (such as within a particular city), some automakers consider shared cars with a level 4 automation level as the best use case. Based on this interpretation, Level 4 vehicles will be allowed to drive autonomously in the area to collect user information on express demand. In addition, there are other preferred application areas depending on the level of automation. Level 1 to 3 vehicles are mainly used for roads and highways, because from a technical point of view, this use case is relatively easy to implement. Technical availability and legal factors are bottlenecks: PricewaterhouseCoopers' Autofacts anticipates that the demand for autonomous vehicles in such large markets as Europe, the United States, and China will vary, but in these regions, customers often hold autopilot technologies themselves. enthusiastic attitude. In addition to technical issues, the development of self-driving cars is currently limited due to lack of a legal framework. Today, there are very few cars on the road with 2 and 3 levels of automation. From a technical point of view, more and more car manufacturers will be able to produce cars of this class, but the legal framework is not yet clear. The current assumption is that even if there is a major technical breakthrough in advance, the market for four-level automated cars will have to be as early as 2022-223. Various automakers have announced that they can produce automobiles with a level 4 and 5 automation level. Automated and shared: If you combine the two trends of sharing and automation, you get four dimensions of travel: Can't share and can't autopilot Already able to share not yet able to autopilot Failed to share but can autopilot Already able to share and autopilot The most popular transportation today is still a self-drive private car (hence "can't share and not drive"). However, self-driving shared cars (in other words, "already shared but not yet able to drive automatically") are becoming increasingly popular. Self-driving private cars ("not shared but can be automatically driven") are not yet available, but may change radically in the coming years. At the same time, this will also paving the way for the sharing of driverless cars ("sharing and autopiloting") and the integration of the two dimensions of autopilot and sharing. In driverless mode, the time-varying rental car and the online booking car are technically the same, because they do not require the user to drive. However, there are still some differences between the two business models. Vehicle rental time users will choose a specific brand for a particular model, while online booking users will be interested in specific transportation services from a specific brand service provider. Individual users will certainly switch between the two modes, which means that both modes have obvious commercial potential. Urban and Rural: It is foreseeable that the main application areas for these two types of travel sharing will be urban areas. Robotaxi ("shared and self-driving") is particularly suitable for promotion in cities. Prevent traffic accidents, reduce congestion at the same time, and increase road traffic efficiency, so that it can accommodate rising traffic flow. The use of private cars, whether automated or unmanned, is still mainly concentrated in rural areas. In cities, the inclusion of these private cars in the widely used Robotaxi network will reduce the use of private cars. For those consumers who still value their own vehicles, automatic cars are often a symbol of status. Progressive vehicle differentiation: Although the mode of travel by motor vehicle has changed, we still believe that there will be gradual differentiation in size and subdivision. There are shared cars in high-end cars and flat car subdivisions, but due to the predominant use of cities, these cars are likely to be small cars with less seats. In contrast, self-driving private cars are often large cars, especially high-end cars. However, the future of automobiles will not only be a matter of sharing and automation, but also a matter of interconnection and motorization. Due to the rapid development of electric drive systems, it can be predicted that the vast majority of Class 4 and Class 5 self-driving cars will be electric cars. At the same time, this also heralds a greater degree of interconnection possibilities, in part because the large-scale deployment of electric vehicles will become a precondition for the widespread use of self-driving cars. In addition, the concept of connected cars also covers various automotive and interconnected services. How will the global automotive market change? Based on the concept of personal mileage, we calculated the percentage of electric vehicles that accounted for the total sales of new vehicles. We originally studied the aggregation factor to indicate the average person-carrying rate per vehicle (more detailed explanations of this concept will be given later in this article). This factor helps us convert personal mileage into vehicle mileage. In turn, we can also use this factor to determine the amount of electric vehicles needed for annual mileage. Through a certain mode of vehicle ownership turnover and its changes, we are able to calculate the new car sales required by the EU, the United States, and China. The universal sharing of travel modes and the changes in the level of automation involved have a positive impact on the advent of the electrification era. The choice of vehicles at the time of travel will change: The changing trend of user roles shows that by 2030, automatic and shared travel will become more common. This will not only affect the driving style but will also affect the owner. Europe Currently, less than 1% of all travels in Europe use shared services. By 2030, with an increase in compound annual growth (2017-2030), which is expected to exceed 20%, this proportion will increase significantly, and the proportion of total mileage in the second half of 2020 will reach more than 10%. Around 2022, autonomous vehicles will be available. These first generation fully autonomous cars may focus primarily on sharing concepts because, as previously mentioned, this is their preferred area of ​​use. This will greatly promote shared services, because relying on "human cost factors" will not work. From 2022 to 2030, the annual average growth rate of market share derived from the concept of autonomous sharing can reach over 70%, and by 2030 it will account for more than 25% of the travel mode. According to our forecast, by then, the proportion of traditional self-driving cars in all car mileage is far below 50%. At the same time, the proportion of self-driving car mileage to all car mileage can reach more than 40%. United States In the United States, only 1% or more of personal vehicle mileage is currently shared. This proportion may exceed 5% by 2021 and may reach as high as 33.5% by 2030. At that time, the share of unmanned shared cars could be close to 10%, and self-sharing cars could approach 24%. And, by 2030, the mileage of autonomous vehicles in the United States will approach 36%. China In China, the proportion of shared cars may increase further. At present, some cities have restricted the registration of new cars, which is bound to have a positive impact on the promotion of shared car concepts. We believe that by 2030, the proportion of shared cars used in personal mileage will likely exceed 45%. In China, self-driving cars will be rapidly promoted due to the high level of acceptance and demand. By 2030, autonomous driving will account for nearly half of all vehicle mileage. Conservative forecast: future travel methods are affected by various factors and cannot be accurately predicted. The legal and technical conditions have been constantly changing, bringing about a certain degree of freedom in adapting to emerging travel modes. Consumers' attitudes and acceptance of autonomous sharing of cars depend on their future development. Although we can ensure that the direction of evolution towards autonomous sharing is clear, unforeseen key events (such as fatal accidents caused by technical failures) may have a long-term impact on acceptance and demand levels. As a result, PricewaterhouseCoopers Autofacts decided to make conservative forecasts and optimistic forecasts. Under conservative estimates, the penetration of vehicles using autonomous technology will vary from 10% to 15% depending on the country and region. In this case, the principles and levels of consumer acceptance of technology and laws will not be repeated. Optimistic forecasts: Open forecasts predict that autonomically driven cars will maintain extremely high adoption rates in the future. In this case, by 2030, the proportion of all self-driving cars in personal mileage will reach more than 60%. Neither consumer demand nor legal and technical requirements will create any obstacles to the development of this new mode of travel. Personal miles and car miles will increase: Personal miles and car miles are a key point in our model. As mentioned above, the degree of correlation between these two numbers depends on the average manned rate of the vehicle. When we study sharing and automation issues, we call them aggregation factors. Using this factor for statistics, the carrying rate of shared vehicles (such as UberPOOL) is relatively high. In one country, the basic starting number for describing mobility is personal mileage. According to people's use of vehicle behaviors to divide travel modes, mileage forms a basis for calculating and calculating vehicle ownership. We can also indirectly calculate the sales volume of new vehicles. Reasons for increased personal mileage include population growth and motorization rates, as well as relative and absolute travel cost changes. The prediction of this and other macroeconomic and social factors determines the credibility of the increase in personal mileage. In this study, the author will assume that the economic development in the three regions studied is basically stable. By automating the sharing of cars, more and more people will participate in motorized traffic. Older people, physically handicapped people, low-income people, and people without a driver's license, especially children and young people, can actively participate and help increase personal mileage. Europe In Europe, the current passenger vehicle mileage is nearly 3.7 trillion kilometers. The average occupancy rate per vehicle is 1.3, which is equivalent to nearly 4.8 trillion annual mileage per year. The manned rate varies according to the mode of travel. For shared vehicles, we first assume a relatively high aggregate factor. United States At present, the US passenger vehicle travels nearly 4.7 trillion kilometers each year. With an average occupancy rate of 1.3 people per vehicle, the total length of passenger vehicles per year reaches 3.59 trillion kilometers. The future vehicle mileage may increase up to 6 trillion kilometers. China At present, China's total mileage is still far behind Europe and the United States. Personal mileage is about 3.0 trillion kilometers. Mileage will increase significantly in the coming years and it may exceed the United States by 2030. The intensity of vehicle use will increase: However, to calculate the inventory quantity and the sales volume of new vehicles, further data are needed, namely the annual mileage of the vehicle and the mileage during the entire life-span at the time of retirement. Through these two figures, we can get the vehicle replacement rate. Over time, the mileage of these four modes of travel will increase. The reasons for this include the advancement of electrification and the related simplification of the driveline. Future vehicle maintenance needs and accident rates will decrease. This means that during the planned mileage, the probability of failure will decrease. When studying the turnover rate, in addition to the total mileage, the relevant data of annual mileage should also be considered. Annual mileage varies greatly, depending on the mode of travel. The use of shared cars far exceeds that of private cars, so the mileage is higher each year. If this effect is combined with autonomous driving technology, more people will use the shared self-driving car, which will lead to further increase in annual mileage. In addition to the promotion of the idea of ​​using automatic cars, the journey of private cars will also lead to a significant increase in mileage, because both shared autos and private autos can carry passengers to a certain location on demand. The combination of annual mileage and actual mileage can be used to calculate the average vehicle life expectancy and the resulting replacement rate. The situation is very different for shared and private cars. Since the time of purchase of the car, the current use of private cars is far more than ten years. The shared concept of shared cars has a much shorter half-life. Because consumers have high expectations for the level of shared car services, such cars must be technically and visually friendly to consumers. The increase in annual mileage and the reduction in total vehicle mileage means that the replacement rate of self-driving cars will be much higher than that of private cars. The amount of vehicle ownership will be reduced: dividing the individual year mileage by the average number of years of the vehicle will result in the number of vehicle ownership. In this article, all travel modes have different annual mileage. Ownership represents the number of vehicles required to guarantee mileage. Europe At present, there are more than 280 million vehicles in Europe, almost all privately owned and used. The percentage of transitions to autonomously shared travel shows that by 2030, the number of possessions may drop to more than 200 million vehicles. At the same time, due to the higher utilization rate of shared autonomous driving, the number of vehicles owned by the ownership can generate higher mileage, which will exceed 4.2 trillion kilometers. By 2030, the ownership of self-driving private cars may drop by 110 to 170 million vehicles. By 2030, the mileage of 27 million self-driving cars (13% of the total holdings) may account for over 40% of all personal mileage. United States Various modes of travel may result in a decrease in holding capacity from 270 million vehicles in 2017 to 212 million vehicles in 2030. Nearly 7% of the reduction in holdings is due to the use of shared vehicles. By 2030, nearly 10% of vehicles will be able to drive autonomously. China At present, China has about 185 million vehicles. However, the strong upward trend in mileage means that the inventory capacity will subsequently fall below the levels in Europe and the United States. The peak capacity may be more than 310 million units, and it will drop to 280 million units by 2030. During the transformation of the automotive industry, car sales will increase, but then may decline. To calculate the sales of a new car, it is necessary to understand the estimated amount of possession, annual average mileage and total mileage. With the last two figures, we can calculate the vehicle replacement period. By dividing the replacement period by the amount of possession, new vehicle sales can be derived. New car sales in all countries and regions studied will increase. The reasons are not the same. The European and U.S. markets are slower to grow, with only a single digit growth rate. On the other hand, due to population growth, increased mobility, and accelerated urbanization, Chinese new car sales still maintain a strong growth momentum, although new car sales are affected by macro-control to ensure it. The city will not be overly congested. In addition to government and economic factors, changes in travel behavior will also have a significant impact on the sales of new cars in the future. As shown in the above chart, the auto-driving shared car form is updated faster, which will have a positive impact on new car sales. Europe By 2030, new sales of light vehicles may increase from the current 17 million to more than 24 million. As early as 2025, total new car sales may include 2 million unmanned cars. By 2030, this figure will grow steadily, reaching nearly 12.5 million vehicles. This means that one in every two new cars is fully autonomous, and this will complete the transition to the new normal of “eascy†vehicles. During the study period, shared service demand may create 30% (equivalent to more than 7.3 million) new car sales. However, we believe that service differentiation is more likely to lead to an increase in popular models than decrease - but under certain conditions. United States Various modes of travel may result in a decrease in holding capacity from 270 million vehicles in 2017 to 212 million vehicles in 2030. Nearly 7% of the reduction in holdings is due to the use of shared vehicles. By 2030, nearly 10% of vehicles will be able to drive autonomously. China At present, China has a car ownership of about 180 million vehicles. However, the strong upward trend in mileage means that the inventory capacity will subsequently fall below the levels in Europe and the United States. The peak capacity may be more than 310 million, and by 2030 it will drop to 280 million. Automation and electrification are complementary. As mentioned above, the "eascy" model shows that most cars with 4 or 5 levels of autopilot technology will be electric vehicles. The continuous use of self-driving cars will expand the application of electric vehicles. This will lead to a shift in demand from political expediency to customer-centricity. As a first step, self-driving cars will be used primarily for shared services. The self-driving electric vehicle satisfies people's shared needs for low-emission and convenient transportation when they travel, and will become an ideal tool for city travel. Vehicles in Europe are currently mainly classified into Level 0 or Level 1. At level 2 there are some vehicles, such as the Mercedes E-Class with the "smart driving" system, and some with Class 3, such as the new Audi A8. We assume that the auxiliary level (level 1) is first extended to partially autonomous (level 2) vehicles. On the other hand, autonomy (level 3) will play a relatively small role, because the focus of the next few years has been on the autonomous vehicles (level 4) to meet the application of shared services. PwC Autofacts sees regulation as another influencing factor in electrification. In order to quantify the "electricalization" dimension, we have chosen an existing model that focuses on the formulation and compliance of carbon dioxide targets. In addition to political and legal regulations, the integration of concepts of electrification, autonomy, and sharing can have a positive impact on the sales and retention of new electric vehicles.æ ¹æ®è‡ªä¸»é©¾é©¶å’Œå…±äº«æ±½è½¦çš„æ™®åŠæƒ…况,到2030年,欧洲新车销售ä¸å†…燃汽车的比例å¯èƒ½ä¼šé™è‡³5%以下。åŒæ—¶ï¼Œæ¯2辆新车ä¸å°±æœ‰1辆以上å¯ä»¥æ供纯电力驱动。在回顾期内,混åˆåŠ¨åŠ›è½¦è¾†çš„é‡è¦æ€§å°†æŒç»ä¸Šå‡ï¼Œåˆ°2030å¹´å°†å 欧洲所有新车销é‡çš„40%以上。 å¯¹æ±½è½¦ä»·å€¼é“¾äº§ç”Ÿä»€ä¹ˆæ ·çš„å½±å“? æ£å¦‚æˆ‘ä»¬é¢„æµ‹çš„é‚£æ ·ï¼Œæ±½è½¦è¡Œä¸šçš„å…¨é¢å¿«é€Ÿé‡ç»„将对整个行业åŠå…¶ä»·å€¼é“¾äº§ç”Ÿæ·±è¿œçš„å½±å“。为了应对2030年以åŽçš„å‘展趋势,基础结构和价值观念必须迅速改å˜ã€‚如果想ä¿æŒæˆåŠŸï¼Œåˆ¶é€ 商和供应商都必须以客户为导å‘æ¥åšæŒåˆ›æ–°ã€‚本报告å¯ä»¥ä¸ºåˆ¶é€ 商ã€ä¾›åº”商ã€æ±½è½¦è´¸æ˜“以åŠä¿é™©å…¬å¸å’Œå…¶ä»–金èžæœåŠ¡æ供商æ供战略和ç†å¿µå¯ç¤ºã€‚æˆ‘ä»¬ç ”ç©¶çš„æœ€åˆç„¦ç‚¹æ˜¯ä¼ 统汽车行业。 ç ”å‘预算需快速é‡æ–°åˆ†é…:如上所述,åªæœ‰ä¸€å®¶æ±½è½¦å…¬å¸â€”—特斯拉,出现在全çƒå大最具创新性公å¸ä¹‹ä¸ã€‚å…¬å¸è§„模固然é‡è¦ï¼Œä½†æ›´é‡è¦çš„是投资类型。为了应对汽车行业é‡ç»„带æ¥çš„æŒ‘æˆ˜ï¼Œåˆ¶é€ å•†å’Œä¾›åº”å•†éœ€ç²¾å‡†å¿«é€Ÿé‡æ–°åˆ†é…é¢„ç®—ã€‚ç ”ç©¶å’Œç ”å‘需关注软件和æœåŠ¡ï¼Œè€Œä¸”还è¦å…³æ³¨åˆ¶é€ çš„å¯è¡Œæ€§å’Œè½¦è¾†çš„模å—化。软件需æ高产å“的性能,æœåŠ¡åˆ™éœ€ä¸ºå®¢æˆ·æä¾›é¢å¤–的功能,其对用户的å‹å¥½æ€§è¦æŒç»æ”¹è¿›ï¼Œè¿™äº›è¦æ±‚必须能çµæ´»åœ°é›†æˆåˆ°ç¡¬ä»¶ä¸ã€‚ 2020年到2025年,公å¸é¡»ä½œå‡ºä¼ä¸šé•¿æœŸç”Ÿå˜çš„战略决定:汽车行业的「eascyã€è½¬åž‹å°†è¿œéžæ˜“äº‹ã€‚ä¼ ç»Ÿçš„åˆ¶é€ å•†å’Œä¾›åº”å•†åœ¨æœªæ¥å‡ å¹´å°†éžå¸¸è„†å¼±ã€‚一方é¢ï¼Œä»–们将ä¸å¾—ä¸é¢å¯¹åˆ©æ¶¦çŽ‡ä¸‹æ»‘的趋势,å¦ä¸€æ–¹é¢ï¼Œä»–们åˆéœ€åœ¨ç”µåŠ¨æ±½è½¦å’Œæ–°å…´å®¢æˆ·å¯¼å‘型创新方é¢ä½œå‡ºæ›´å¤§çš„æŠ•èµ„ã€‚å†…ç‡ƒæœºï¼Œå°¤å…¶æ˜¯å‡ åå¹´æ¥æ”¯æ’‘汽车工业å‘展的内燃机将会过时。与æ¤åŒæ—¶ï¼Œè¶Šæ¥è¶Šå¤šçš„æ–°ç«žäº‰å¯¹æ‰‹å°†æ¶Œå…¥å¸‚åœºï¼Œä¼ ç»ŸåŽ‚å•†çš„å‘å±•å°†æ›´åŠ å›°éš¾ã€‚é¢„è®¡åˆ°2020-2025年,这些竞争趋势将达到白çƒåŒ–的状æ€ï¼ŒåŒæ—¶è¿™ä¹Ÿæ„味ç€å¯¹äºŽåˆ¶é€ 商åŠå…¶ä¾›åº”商而言,2020-2025å¹´å°†ä¼šæ˜¯å…³é”®æ€§çš„å‡ å¹´ã€‚ è¿™ä¸ä»…关于汽车,而且更关乎出行方å¼ï¼šåˆ¶é€ 商和供应商若åªç»§ç»ä¸“注于汽车的生产和销售,在汽车行业é‡ç»„的大背景下,它们的管ç†å°†ä¼šå˜å¾—异常困难。在「eascyã€æ—¶ä»£ï¼Œå•†ä¸šæ¨¡å¼çš„æ ¸å¿ƒï¼Œä¸å†åªæ˜¯äº§å“,而将是出行æœåŠ¡ã€‚å‡å¦‚å…¬å¸æƒ³ç»§ç»è‡´åŠ›äºŽæ»¡è¶³å®¢æˆ·ä¸æ–å˜åŒ–的期望,这将是唯一的途径。将“硬件â€ï¼ˆå³è½¦è¾†ï¼‰ä¸Žâ€œè½¯ä»¶â€ï¼ˆå³æœåŠ¡ï¼‰è”系起æ¥æ˜¯éžå¸¸é‡è¦çš„。 å°¤å…¶æ˜¯å¯¹åˆ¶é€ å•†è€Œè¨€ï¼Œå®ƒä»¬å°†å¿…é¡»åšå‡ºè‡³å…³é‡è¦çš„抉择,è¦ä¹ˆç»§ç»åšè§„模车队æ供商,è¦ä¹ˆåšæœåŠ¡æ供商。对于æŸäº›åˆ¶é€ 商,它们转型的æ£ç¡®é€”径å¯èƒ½æ˜¯ä¸“注于这两个领域ä¸çš„一个,而å¦å¤–一些则有å¯èƒ½åœ¨å¤šæ ·åŒ–的过程找到其å‘展的契机。尽管é¢ä¸´ç€å·¨å¤§çš„挑战,但ä»æœ‰ä¸€äº›ä»¤äººä¹è§‚çš„è¶‹åŠ¿ï¼šåˆ¶é€ å•†è¿›å†›å‡ºè¡ŒæœåŠ¡é¢†åŸŸï¼Œå°†ä¸ºå…¶å¼€è¾Ÿæ–°çš„收入æ¥æºï¼›ä½†ä¸Žæ¤åŒæ—¶ï¼Œæ±½è½¦ç”Ÿäº§å’Œé”€å”®çš„æ ¸å¿ƒä¸šåŠ¡å°†ä¼šé¢ä¸´æ›´å¤§çš„压力。 SHENZHEN CHONDEKUAI TECHNOLOGY CO.LTD , http://www.siheyidz.com